IBM Fan Bin Talks about Blockchain Application in Financial Industry: Technology is in the Stage of Immature but Rapid Development

IBM, as one of the giants of the early deployment of blockchain commercial applications, has had more research on blockchain business in the areas of cloud services, financial services, and other areas. Prior to this, Lei Fengwang (searched by the "Lei Feng Network" public number concerned) Reported on emerging cloud services of IBM's "blockchain as a service". Today, at the sharing event held by Titanium Media, Fan Bin, General Manager of the Greater China Area Banking Business Unit of the Global Block Group of the IBM Blockchain Research Group shared the application of IBM in the financial industry:

I: Excerpts from the IBM Global Blockchain Application Report

Two: blockchain industry application scenarios and obstacles

III: The application of blockchain in the financial industry

IBM Global Blockchain Application Report: Eliminating Trade FrictionAccording to reports, in the entire banking industry, IBM has established an organization named IBV "IBM Business Value Institute" from an overall perspective. The organization recently completed an unpublished report, and Fan Bin revealed that the report is called "Full speed ahead - rethinking the corporate ecosystem and economic model with blockchain".

In this report, IBM put forward several research results. The first point is that in fact, for centuries since mankind, some global trade, or some global development, has been based on the methods of creation of wealth to promote human development. But in the course of human development, one of the most important things - we define it as friction. Friction can hinder some of human development. Therefore, in fact, the long process of human progress is a process of eliminating friction.

And at the moment,

We believe that the most important friction comes from the friction of information, the friction of interaction, and some of the challenges that innovation poses to the efficiency of frictional operations.

One of the most important is the asymmetry of information, resulting in the parties to the transaction can not get the same information. Even in the era of big data, the wrong information will make them more disadvantaged.

The second aspect is the friction of interaction. The main reason for interaction friction lies in doing transactions. We do separation. For example, the cost of a transaction, the operating cost of a business is related to its complexity, and some complicated businesses may have many transactions back and forth in the processing of counterparties, and as the scale increases, the resources to be managed, including intermediaries, Increase and increase, so that in almost all cases, complexity will erode your gains. The longer the process, the greater the possibility of erosion of revenue, and the result is a higher cost to the end user. And there is a degree of separation in the interaction friction. With the flattening of the world, the digital platform will connect together completely different parties, and the distance will be greatly shortened. Therefore, the main goal of the disintegration of these flexible trading competitors is to separate. There must be some progress in terms of degree.

In the predicament of these frictions, IBM Global believes that the research on the attribute framework of the blockchain exerts force in the following aspects to promote some developments in the entire society by reducing friction.

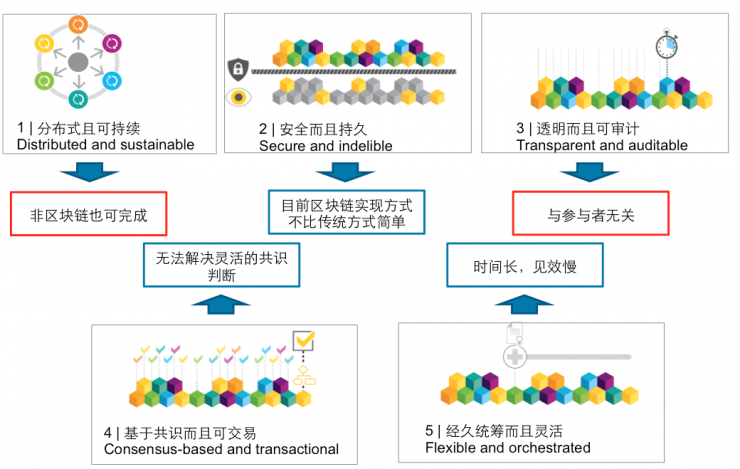

The first aspect is distributed and sustainable, because the general ledger will be updated continuously with each transaction, can be shared among all transactions, and then can be selectively replicated with participants in near real time , Protecting privacy through encrypted technology. Of the features in the blockchain, there is one that is particularly important: because of the fact that part of the billing is commonly recognized. Many of the original things, such as in the bank, would not be available in the unified block book of the blockchain for the reconciliation, omitting many related things and costs.

The second point is safety and long-lasting. It is through this password that the transaction can be firmed and verified, and through this allows to view the relevant part of the account itself. Once this condition is agreed, the participant cannot tamper with the transaction history, and only the new transaction correction record can be used. This feature is a function of trust for security and durability, and once a block is made, it can be viewed for the block, and of course, under the control of the corresponding authority, and cannot tamper with the previous transaction.

There is consensus and it is tradable. In this case, all participants in the relevant network must agree and the transaction is effective. This is achieved through a consensus algorithm. The consensus algorithm is actually the most critical factor in maintaining the existence of the entire blockchain in the entire blockchain and continues to develop. The transactions or assets established by the blockchain are all achieved through this consensus transaction, so we can see that there are many such consensus mechanisms: POW, POS, Byzantine's algorithm...

These points, from the perspective of IBM, believe that within the enterprise-level blockchain, IBM has done some research locally and made some analysis on the business scenarios followed by the blockchain.

When we select a business scenario, we may first ask why we trust, who we trust, what trust we rely on, and what is the content of trust?

From the perspective of this analysis, we have to find out the business scenario basically to judge through these several aspects, this application or that this kind of scene is suitable for the traditional implementation way or the way suitable for the blockchain.

SWIFT, also known as the "Global Banking Financial Telecommunication Association", is an international cooperative organization of international banks. It was established in 1937. Most of the banks in most countries in the world currently use the SWIFT system.

In this chart, we have analyzed a lot of cases from high to low according to the four parts just now. So far, in fact, we have analyzed the cases we can publicly see, including traceability, and the second is credits. From the results of our research, Bitcoin is still the best application in the blockchain.

And for the other things that we currently do here, except for colored coins, the point exchange may be done by everyone. Several other parts, including bills platform, supply chain financing, cross-bank transfer, we currently have proof of concept in many banks, but it is actually biased towards a higher degree of trust - because it is his asset ownership By. Bitcoin is actually trusting who, why it trusts, and what aspects of trust and trust are in a relatively low position. This is why we think Bitcoin's application is more natural.

In addition, why does the point-switching application do more in the current application of many blockchains? In this part of the credit exchange, why trust, trust, and what trust and trust are based on, some of which are at a level below the level of comparison, can be supplemented by blockchain technology, or enhanced to achieve it A more favorable position.

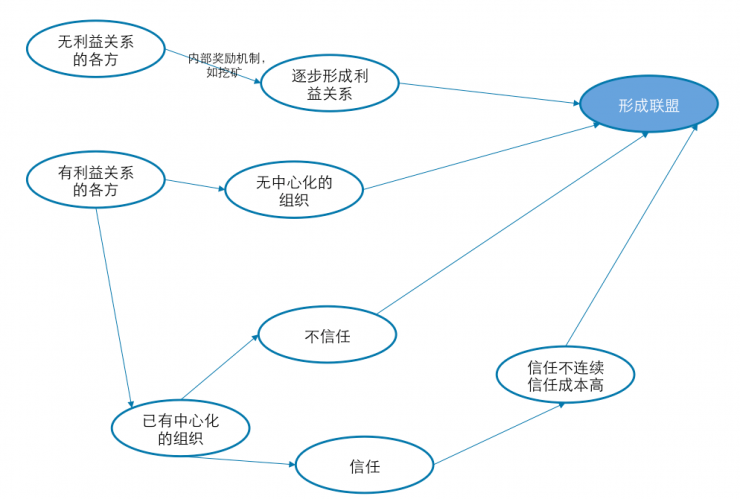

As shown in the following figure, we can see that in several respects, if there are no interested parties and gradually form a number of interest relationships and form alliances, this is an approach. However, this kind of practice is actually under real conditions. In addition to applications like Bitcoin similar to this kind of application, it is basically meaningless in the applications we currently see, and it lacks a relatively good consensus mechanism. A big part of Bitcoin's success lies in its consensus mechanism.

In the second scenario, we can see that there are parties with interests and it is a non-centralized organization. Under such circumstances, we currently find a lot of commercial applications, such as similar to UnionPay, similar to industry associations or industry associations. In this case, if we can find interested parties, Non-centralized organizations are more likely to form alliances through blockchains, but are not easily discoverable in existing business scenarios.

The third possibility, or the third scenario, is that there are interested parties and there are already centralized organizations. However, these centralized organizations, or these participants, do not have special trust. In fact, this can also form a coalition, but what is the disadvantage? In the current situation, it is very difficult for us to break. Because many financial institutions are already within a centralized organization, it is difficult to break this current approach.

In this case, we believe that there are interested parties, and there are centralized organizations, and that these organizations are more trustworthy—on the basis of trust, because the entire business process is the overall process of an N2N. Therefore, trust is not continuous, perhaps for example as trade finance. I may trust in some chains of trade finance, such as payments or in the chain of other guarantees, but besides this, it may be difficult to trust, or the cost of trust may be high. .

In this case, alliances can also be formed. But what are the disadvantages? Because the coalition formed by this method is not particularly easy, that is to say, when these situations are seen to be used for context analysis, in addition to the business model that Bitcoin has already formed, In many other situations, it depends on discovery.

Blockchain application in the financial industry: very immatureAt present, our blockchain is not yet mature and is in an immature and rapid development stage.

In April and May of this year, IBM helped some foreign banks to do POC (Proof of Concept) in asset transactions, while also doing some POC on the liquidation of some stock exchanges. Everyone has a certain degree of consensus on the use of blockchain technology in the inter-bank liquidation and has basically reached a general approach.

On the whole, in the current development path of blockchain, we admit that it is very immature, but we have done POC on many different business scenarios when we discussed it with Chinese domestic financial institutions. Many analysts say that the technology of the blockchain is actually the most relevant and is still in the financial industry.

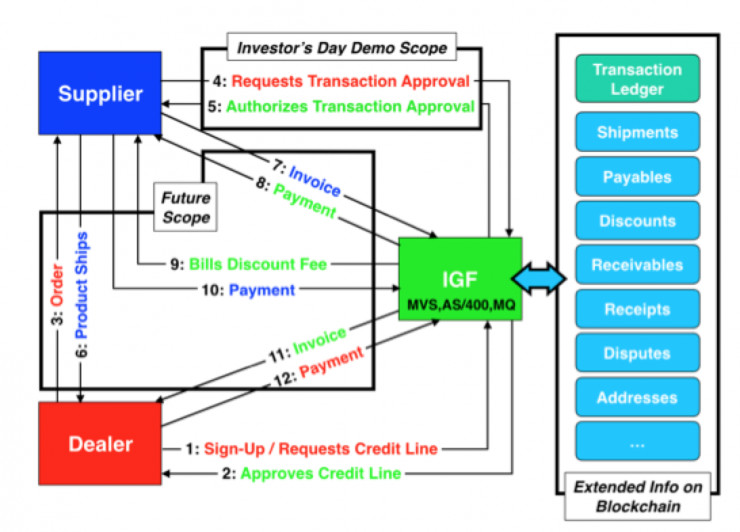

The example I shared today is that in this case, IBM has made a blockchain production. The department introduced is IBM Global Finance. It is actually doing finance. We will give you a brief introduction here.

This department manages about 44 billion credit lines annually, handles 2.9 million invoices each year, and then has business contacts with about 4,000 partners in the world. It will probably handle 25,000 highly time-consuming dispute payments each year. Due to these disputes, companies will use about 100 million U.S. dollars of liquidity each year, because this department is mainly responsible for the flow of funds throughout IBM. What is the source of the account? During the entire transaction process, we will encounter a situation, such as a hardware product or a service. Take the hardware product as an example. I think that I have made a server which has been delivered to the downstream IBM. A certain business department, I will ask for payment, and invoice, but often due to a variety of reasons, the downstream departments can not immediately find out whether this thing has arrived, or that has been received As a result, there will be a large delay after the invoice is issued.

This application of IBM actually reduced the amount of disputed accounts that could have been resolved in the past 40 days to an average level of about ten days. Well, almost all of the original 100 million U.S. dollar liquidity was released. Moreover, many of the partners on this blockchain platform can clearly understand the operating mode of the entire chain of funds and can provide a very rich view of their general ledger and operational data. Some time ago, the scandal of a bill occurred in a certain bank and caused a lot of losses. We are currently helping him with a POC at this financial institution. The main problem in this proof of concept is to extract some related business scenarios - where the business pain points are, and then to be able to achieve through blockchain technology.

In general, in fact, IBM should be stronger from the technical aspects: basic technologies, technology platforms, and the above consensus algorithm, encryption technology... But I think another very important point is that we are actually doing business consulting. Service, through modeling or what kind of summarizing and summarizing method, can pack the pain point of the business into a solution that the technology can solve. This is the most important skill.

Automotive Diagnostic Connectors And Cables

We make OBD connector with terminal by ourselves, soldering type and crimping type are both available. Such as 16pin obd connector. OBD1, OB2, J1939, J1708, J1962, etc. Also molded by different type, straight type or right-angle type. The OBD connector cables used for Audi, Honda, Toyota, BWM, etc. We have wide range of materials source , also we can support customers to make a customized one to replace the original ones.

Automotive Diagnostic Connectors And Cables,Obd Connectors,Reliable OBD Connector,Black OBD Connector,OBD Diagnostic Cable,OBD2 Connectors

ETOP WIREHARNESS LIMITED , http://www.oemmoldedcables.com